Introduction

In recent months, global bond markets have been shaken by a rise in bond yields, which has had significant implications for investors. For years, investment-grade bonds—those issued by financially stable corporations or governments—have been seen as the cornerstone of conservative, steady-income portfolios. However, with the uptick in bond yields, particularly in the face of rising inflation and central bank interest rate hikes, many are questioning whether investment-grade bonds can still be relied upon as the safest, most stable investment vehicle.

This article explores the dynamics driving rising bond yields, the impact on investment-grade bonds, and whether these bonds remain a reliable option for risk-averse investors. By analyzing the factors influencing bond yields, evaluating the risks and rewards associated with investment-grade bonds in the current economic climate, and considering alternative investment options, we will assess whether investment-grade bonds continue to be the preferred choice for conservative investors.

1. Understanding Bond Yields and Investment-Grade Bonds

Before delving into the impact of rising yields, it is crucial to understand what bond yields are and what qualifies as an investment-grade bond.

A. What Are Bond Yields?

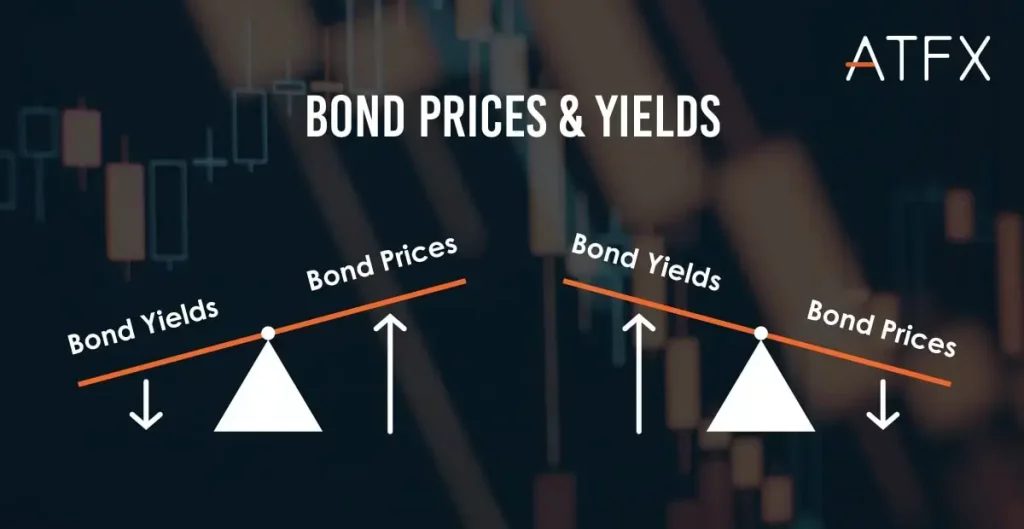

Bond yield refers to the return an investor can expect from holding a bond to maturity, expressed as a percentage of the bond’s face value. Bond yields are inversely related to bond prices, meaning that as bond prices fall, yields rise, and vice versa.

- Yield to Maturity (YTM): This is the total return an investor can expect if the bond is held until its maturity date.

- Current Yield: This is calculated as the bond’s annual coupon payment divided by its current price.

The rise in bond yields over recent months has been primarily due to higher inflation expectations, tighter monetary policies from central banks, and increasing concerns about economic growth.

B. What Are Investment-Grade Bonds?

Investment-grade bonds are those with a high credit rating from rating agencies like Standard & Poor’s (S&P), Moody’s, or Fitch. These bonds are issued by governments or corporations with strong credit profiles, implying that they are less likely to default on interest or principal payments.

The credit ratings for investment-grade bonds range from BBB- (S&P or Fitch) or Baa3 (Moody’s) to AAA. These bonds are considered safer than lower-rated (junk) bonds, though they offer lower returns in exchange for reduced risk.

Investment-grade bonds are traditionally seen as a stable source of income for conservative investors, particularly in a low-interest-rate environment. However, the rise in bond yields has raised questions about the future stability and appeal of these bonds.

2. The Current Environment: Why Are Bond Yields Rising?

Understanding the factors driving the rise in bond yields is essential to evaluating whether investment-grade bonds remain a safe and stable choice.

A. Inflationary Pressures and Central Bank Policies

One of the key factors contributing to rising bond yields is persistent inflation. Since 2021, inflationary pressures have been escalating globally due to a combination of factors, including:

- Supply Chain Disruptions: The COVID-19 pandemic severely disrupted global supply chains, creating shortages of goods and raw materials. This, in turn, pushed up prices.

- Increased Consumer Demand: As economies reopened and stimulus packages spurred consumer spending, demand for goods and services surged, adding further inflationary pressure.

- Energy Prices: Rising energy costs, particularly for oil and natural gas, have been a significant driver of inflation in many countries.

In response to rising inflation, central banks—especially the U.S. Federal Reserve—have taken a more hawkish stance by raising interest rates and signaling further tightening of monetary policy. Higher interest rates lead to higher bond yields because newly issued bonds must offer more attractive yields to compensate for the opportunity cost of holding older bonds with lower yields.

B. Government Debt and Fiscal Stimulus

The aftermath of the pandemic has also seen governments running large fiscal deficits to finance stimulus packages, social programs, and infrastructure spending. Increased government borrowing can push bond yields higher, particularly if markets begin to fear that excessive borrowing may lead to inflation or a weakening of fiscal discipline.

The U.S. Treasury, for example, has issued substantial amounts of debt to fund stimulus measures, which can put upward pressure on yields as the supply of bonds increases. Higher government borrowing can make it more expensive for investors to buy bonds, thus raising the yield required to entice investors.

C. Market Sentiment and Economic Outlook

The rise in bond yields can also be attributed to shifting market sentiment. As the global economy begins to recover from the pandemic, investors are recalibrating their expectations for growth, inflation, and interest rates. If investors expect stronger economic growth and higher inflation, they will demand higher yields on bonds to offset the eroding impact of inflation on fixed coupon payments.

Rising bond yields can also reflect market skepticism about the sustainability of economic recovery. If investors are concerned that central banks may need to continue raising rates to combat inflation, bond prices can fall (which causes yields to rise), as investors demand higher returns for holding debt in a higher interest rate environment.

3. The Impact of Rising Bond Yields on Investment-Grade Bonds

The rise in bond yields has significant implications for investment-grade bonds, particularly in terms of their price and the income they generate for investors.

A. Bond Prices and Yield Increases

As bond yields rise, bond prices generally fall. This is because investors can get better returns from newly issued bonds with higher yields, so the price of existing bonds with lower yields must decrease to remain competitive.

For example, if an investor holds a bond with a 2% coupon and market yields rise to 3%, the price of the bond will decrease to reflect the fact that the bond now offers a lower yield than newly issued bonds. This means that, while investors can still hold their investment-grade bonds to maturity and receive the full coupon payments, they may face a paper loss in the short term if they need to sell the bonds before maturity.

B. Decreased Total Returns

For long-term investors in investment-grade bonds, the rise in yields can result in lower total returns. While higher yields may offer more attractive future returns, the capital losses from falling bond prices can offset those gains, especially for investors holding long-duration bonds. In particular:

- Long-Term Bonds: Bonds with longer maturities are more sensitive to interest rate changes. As a result, long-term investment-grade bonds have seen significant price declines as yields rise. This has made them less attractive for conservative investors looking for capital preservation.

- Short-Term Bonds: Short-term investment-grade bonds are less affected by rising yields, as their prices are more stable. However, the lower yields offered by short-term bonds may not provide the level of income that some conservative investors seek.

C. Impact on Income Stability

For investors relying on the income generated from investment-grade bonds, the rising yields can offer both opportunities and challenges. On the one hand, higher yields mean that new investments in bonds can provide better income streams. On the other hand, the income from existing bonds will not increase, and the potential for capital losses may reduce overall portfolio returns.

4. Are Investment-Grade Bonds Still a Reliable Investment?

Given the challenges posed by rising bond yields, the question remains: Are investment-grade bonds still a reliable investment for conservative investors? The answer depends on the investor’s goals, time horizon, and risk tolerance.

A. Benefits of Investment-Grade Bonds in the Current Environment

- Stability and Lower Risk: Despite the potential for price declines in the short term, investment-grade bonds remain a safer alternative to equities, especially during times of economic uncertainty or market volatility. Their predictable income streams make them attractive to conservative investors who prioritize capital preservation.

- Diversification: Investment-grade bonds can help diversify a portfolio by providing a steady income stream that is less correlated with stock market movements. This can help smooth out overall portfolio returns and reduce volatility.

- Higher Yields for New Investors: For those looking to enter the bond market, the rise in yields means that newly issued investment-grade bonds offer more attractive income potential. This could make them more appealing for investors seeking fixed-income securities that provide both safety and yield.

B. Risks and Alternatives

- Capital Losses: Investors holding long-duration bonds or bonds purchased at lower yields are likely to experience capital losses as bond prices fall. This could be a concern for those with a short-term investment horizon or those who may need to liquidate their holdings before maturity.

- Alternatives: With rising yields, other investment options may become more appealing. For instance, short-duration bond funds, floating-rate bonds, and high-yield bonds could offer higher returns in a rising-rate environment. Additionally, dividend-paying stocks and real estate investment trusts (REITs) might also provide a better return potential than investment-grade bonds in a higher interest rate world.

5. Conclusion: Are Investment-Grade Bonds Still the Best Choice?

Rising bond yields have created a more complex landscape for conservative investors, but investment-grade bonds are not necessarily off the table. While the price declines and capital losses associated with rising yields are a concern, investment-grade bonds still offer safety, income stability, and diversification for long-term investors.

However, in the current environment, conservative investors may need to adjust their bond strategies. For those with a short-term focus, shorter-duration bonds or floating-rate bonds may be more appropriate. For long-term investors, the rise in yields offers an opportunity to lock in higher rates for future investments, but investors must be prepared for potential volatility in bond prices.

In conclusion, investment-grade bonds remain a reliable choice for those seeking stability and steady income. However, investors should be mindful of the current market conditions and consider diversifying their portfolios to account for the risks associated with rising yields.

{kind=link}